Mortgages For Contractors: Everything You Need To Know

If you are a contractor in the mortgage industry, navigating the complexities of securing a suitable mortgage can be challenging. A specialized mortgage broker is essential to guide you through the intricacies of contractor mortgages.

As Featured In:

Are You A Contractor Looking For A Mortgage?

Leave your contact details and let our experts call you back to discuss tailor-made mortgage solutions for contractors.

When it comes to mortgages, navigating the process can be overwhelming for anyone. However as a contractor it may feel like deciphering a different language all together. You may have heard people say things like “Contractors face challenges in obtaining mortgages” or “Prepare yourself for a mountain of paperwork.”. Don’t let those rumours discourage you. In this blog post we aim to demystify the process and provide you with all the information about contractor mortgages. Whether you’re a contractor or just starting out as a freelancer, let’s dive into the details of securing your dream home.

Table of Contents

What Is a Final Mortgage Credit Check?

So, you’ve come across the term “contractor mortgages.” Well, while most people are familiar with standard mortgages designed for those with regular salaries, but contractor mortgages are a bit different. They’re specifically designed for individuals like freelancers, consultants, and contractors.

Instead of focusing solely on fixed salaries, these mortgages consider the unique financial situations of independent professionals. At Jones and Young, we specialise in this area. We understand the nuances and intricacies of contractor mortgages, and we’re here to guide you through the process. With our expertise, securing a mortgage tailored to your contractor status becomes much clearer.

So, Can Contractors Get a Mortgage?

Now, onto a burning question many contractors have: “Can I actually get a mortgage?” The short answer? Absolutely. While it’s true that contractors might face different challenges than those on a fixed salary, it’s by no means an impossible task. With the right guidance and understanding of the mortgage landscape, contractors can secure a mortgage that fits their unique financial profile. So, if you’re a contractor wondering about stepping onto the property ladder, rest assured, it’s more than just a possibility.

SPEAK TO MARK FOR EXPERT MORTGAGE ADVICE!

Helping self-employed professionals, contractors, freelancers, and small business owners navigate the mortgage process and get the best possible deal.

Benefits Of Using a Contractor Mortgage Broker?

Let’s take a closer look at some of the benefits of using a specialist contractor mortgage broker to secure your mortgage:

Tailored Advice

As contractor mortgage brokers like us specialise in working with contractors, we fully understand the challenges and intricacies of your profession. This allows us to provide advice that are customised specifically for your circumstances than offering solutions.

Access To Specialised Lenders

Next up, your current debts come under the spotlight. The lender will want to see how much you owe and to whom. Credit cards, personal loans, car finance – everything goes under the microscope. The more you owe, the more cautious a lender might be, as it could impact your ability to meet mortgage repayments.

Time-Saving

Searching for the right mortgage can be time-consuming. A broker can streamline the mortgage application process, doing the heavy lifting for you and ensuring you get the best deal without the hassle.

Negotiation Power

With their industry knowledge and connections, brokers can often negotiate better terms and rates on your behalf and often offer a more competitive mortgage deal.

Understanding of Complex Income Structures

Not only do the income streams vary for contractors, but they often have complex financial setups. A specialised broker can effectively present this to lenders, making your application more appealing.

One of the most common questions we hear from contractors is, “How much can I actually borrow for my mortgage?” Well, let’s break it down step by step:

How Much Can I Borrow For My Contractor Mortgage?

Determine Your Weekly Income: Take your contracted day rate and multiply it by the number of days you work each week. This gives you your weekly income.

Contracted day rate x number of days worked each week = your weekly income

Calculate Your Annual Income: Multiply your weekly income by 48 weeks. Why 48? This accounts for some time off, like holidays or any breaks you might take.

Your weekly income x 48 weeks = Your annual income

Estimate Your Maximum Mortgage Amount: Here’s where it gets interesting. Depending on the lender and your financial health, you can multiply your annual income by 4-4.5 to get an estimate of the mortgage loan you may be eligible for.

Your annual income x 4/4.5 = Your maximum mortgage amount

To estimate the amount you can borrow for your contractor mortgage, calculate your annual income by multiplying your weekly income (day rate × days worked per week) by 48 weeks, then multiply the result by 4 to 4.5 to find your maximum mortgage amount.

Remember, every lender might have their own criteria, but this gives you a starting point to understand your potential borrowing power.

Experience The Jones & Young Difference In Contractor Mortgages

At Jones & Young, we understand the unique challenges faced by contractors in securing mortgages. Our dedicated team specializes in navigating the contractor mortgage landscape, ensuring you have the best shot at not only gaining approval but also securing the most favorable rates.

Will I Need A Larger Deposit?

The truth is, being a contractor doesn’t automatically mean you’ll be asked for a heftier deposit. However, the size of your deposit can be influenced by various factors, including thigs like credit history, the lender’s familiarity with contractor incomes, and the overall strength of your application. While some lenders might ask for a larger deposit due to perceived risks, others are more contractor-friendly and offer similar terms for salaried employees.

The method is to shop around, do your research, and consult with a mortgage broker who understands the contractor landscape; they can guide you to more accommodating lenders and give you a clearer picture of what to expect.

Lending Criteria For Contractors

Mortgage lenders often have a specific set of criteria they look at when assessing contractor applications. Why? Because contractors have a different income structure compared to those in traditional employment.

Now, while mortgage lenders might have a unique checklist, there are some common threads. They’ll typically look at the stability of your contracts, your experience in the field, your earnings, and your credit history. Some might also want to examine the track record of consistent work or even future contract rate commitments. They’ll use these to prove that you’re reliable, to work out your average income.

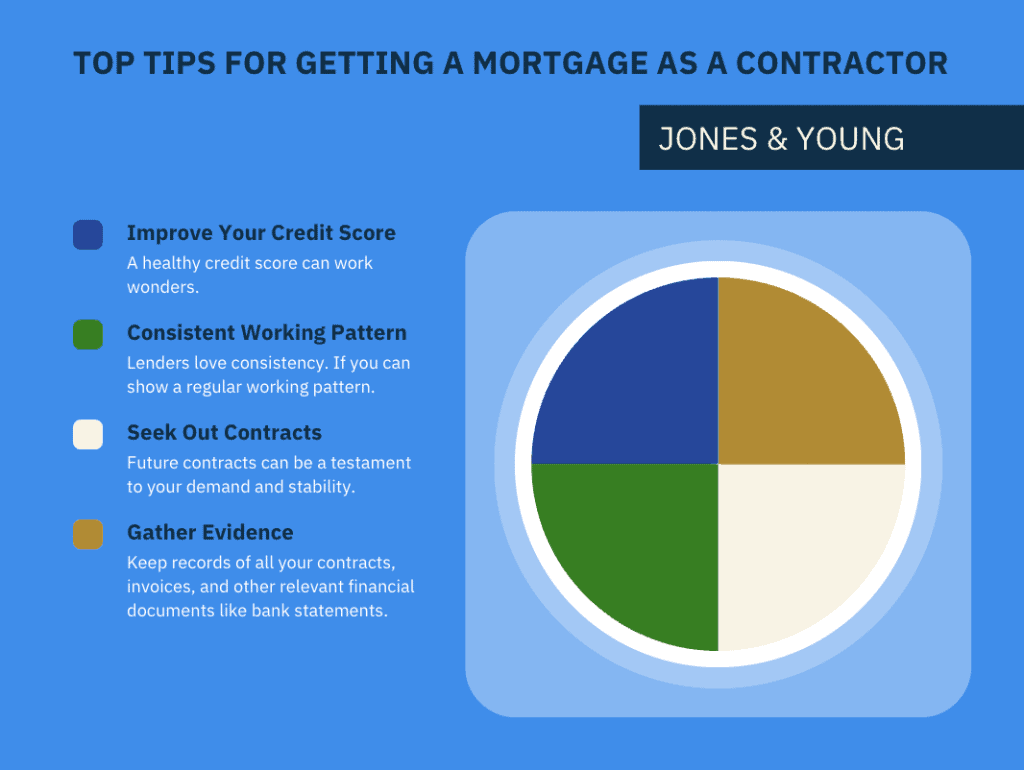

Top Tips For Getting a Mortgage As a Contractor

Navigating the mortgage world as a contractor? While it might seem daunting, there are some ways to boost your chances of getting that approval stamp. Let’s dive into some top tips just for contractors:

Improve Your Credit Score

First things first, a healthy credit score can work wonders. Regularly check your score, clear any outstanding debts, and ensure you’re paying bills on time. A strong credit score can significantly enhance your mortgage prospects and mean the contractor mortgage criteria is sometimes more lenient.

Consistent Working Pattern

Lenders love consistency. If you can show a regular working pattern, even as a contractor, it can be a big plus. It gives them confidence in your ability to keep up with mortgage payments; so, if possible, aim for longer contracts and avoid long gaps between jobs.

Seek Out Contracts

Speaking of contracts, the more you have lined up, the better. Future contracts can be a testament to your demand and stability in the market. It’s like telling lenders, “Hey, I’ve got work lined up, and I’m in this for the long haul.”

Gather Evidence

Documentation is your friend. Keep records of all your contracts, invoices, and other relevant financial documents like bank statements. The more evidence you can provide of your average income and professional stability, the more reassured lenders will feel. If you have a limited company or an umbrella company, this will mean keeping all relevant documentation from this as well.

Remember, while the journey might be a bit different for contractors, with the right approach and preparation, that dream home is well within reach.

Jones and Young: The Contractor Mortgage Experts

When it comes to navigating the intricate world of contractor mortgages, it’s essential to have experts by your side. Enter Jones and Young. We’re not just any broker; we’re specialists in the contractor mortgage area. With years of experience under our belt, we’ve mastered the art of understanding the unique challenges and opportunities contractors face. Whether you’re a seasoned contractor or just starting out, we’re here to guide, advise, and ensure you get the best mortgage deal tailored to your needs.

With Jones and Young, you’re not just getting a specialist mortgage broker; you’re gaining a partner who’s as invested in your homeownership journey as you are. Let’s make your property dreams a reality, together.

Do You Have Any Questions?

Got questions about contractor mortgages? Jones & Young are here to help! Contact us for expert advice tailored to your unique needs as a contractor. Let’s secure your ideal mortgage today!

Clients Speak: Real Success Stories With Jones & Young

Contractor Mortgage FAQs:

We’ve answered some of the most frequently asked questions about contractor mortgages below:

Is it difficult to get a mortgage as a contractor?

Well, it’s a common misconception that getting a mortgage as a contractor is tough. While it’s true that some lenders might be a bit more cautious, many understand the nature of contract work nowadays. As long as you have a steady income and a good credit history, you should be in a good position. Just make sure you have all your paperwork in order and you can secure the most competitive mortgage deal.

Can I get a mortgage if I am a contract worker?

Absolutely! Professional contractors and other contract workers can definitely still get mortgages. The key is to show lenders that you have a consistent income, even if it’s from various sources or by providing your current contract. Keeping detailed records of your contracts and earnings will be very helpful. And remember, every lender has different criteria, so it’s worth shopping around to find the best fit for you.

Can contractors get mortgage in the UK?

Yes, they can! The UK has a robust mortgage market, and there are plenty of lenders who are familiar with the ins and outs of contract and self employed work. Just like anyone else, contractors need to show they’re a good risk, which means having a steady income and a clean credit history. But with the right documentation and a bit of research, contractors in the UK can definitely find a mortgage lender that suits their needs.

How many years do you have to be self-employed to get a mortgage?

This one varies by lender. Some might ask for two or three years of accounts to prove your income, while others might be okay with just one year. It’s always a good idea to check with multiple lenders to see what they require. And if you’ve got a solid track record and a good deposit, that can certainly help your case!

Related Articles

GET IN TOUCH